Such a high level of banking concentration “carries with it a high degree of potential systemic risk,” the IMF report states.

The study also found that too-big-to-fail banks enjoy an unofficial “subsidy” in the form of lower borrowing costs than those enjoyed by smaller banks.

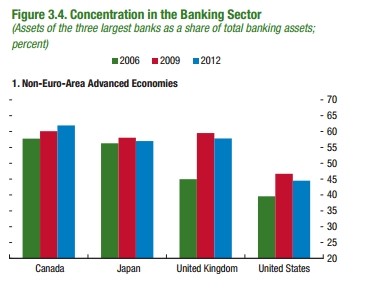

The Global Financial Stability Report found that Canada is one of a handful of countries where the three largest banks -- RBC, TD and Scotiabank -- control more than 60 per cent of all banking assets.

In the U.S., where too-big-to-fail banks brought the economy to the brink of ruin in 2008, banks are far less concentrated; the three largest control about 45 per cent of all bank assets.

And while the U.S., U.K. and other countries have seen concentration lessen since the financial crisis, in Canada the concentration keeps growing.

“The distress or failure of one of the top three banks in a country, for example, could destabilize that country’s entire financial system,” the report says.

If a bank is too large, other banks wouldn’t be able to replace its activities in case it fails, the report says. Too-big-to-fail banks are so integrated into the banking system that other banks would be hit, and confidence in the entire economy would suffer.

The IMF also took a look at an issue that has been concerning some economists -- the unofficial “subsidy” that too-big-to-fail banks enjoy, thanks to lower borrowing costs than other banks.

Because creditors assume that a large bank will be bailed out in case of trouble, they are willing to lend to those banks at lower rates than for smaller banks. And that, in turn, strengthens the large banks and makes them even more important to the economy.

The study didn’t break out how much of a subsidy Canadian banks enjoy from being “too big to fail,” but it did break out the numbers for some larger economies.

In the U.S., the subsidy amounts to $15 to $70 billion per year for the big banks; in Japan it’s in the $15 billion-$70 billion range, and in the euro zone, it works out to $90 billion to $300 billion per year (all figures in U.S. dollars).

Original Article

Source: huffingtonpost.ca/

Author: The Huffington Post Canada | By Daniel Tencer

No comments:

Post a Comment