Warren Buffett doesn't want you to know how his empire is preparing to deal with the disastrous effects of climate change. In fact, he said in a letter released Saturday, he isn't exactly sure this whole "climate change" thing is real, anyway.

Warren Buffett doesn't want you to know how his empire is preparing to deal with the disastrous effects of climate change. In fact, he said in a letter released Saturday, he isn't exactly sure this whole "climate change" thing is real, anyway.In his annual letter to investors in his conglomerate Berkshire Hathaway, the billionaire investor fought back against a proposed shareholder resolution demanding his insurance subsidiaries measure and disclose the risks that climate change poses to their business and how the company is responding to the threat. Buffett compared fears over climate change to the brouhaha around apocalyptic Y2K predictions.

“It seems highly likely to me that climate change poses a major problem for the planet,” the 85-year-old wrote in the letter, released Saturday morning. “I say ‘highly likely’ rather than ‘certain’ because I have no scientific aptitude and remember well the dire predictions of most ‘experts’ about Y2K.”

Insurance companies take on losses after major weather disasters (think droughts, Hurricane Katrina and other big storms), so it makes sense they'd be concerned about climate change. If that's true, why would Buffett say he's not so sure this is real? Because skepticism is better business.

Buffett isn’t denying climate change, but rather using language climate deniers feel comfortable with and will likely cite in future attempts to derail environmental policy. Climate change affects Buffett's business: He owns a Nevada utility that has fought and won against solar development in that state, and his railroad, Burlington Northern, in large part depends on the demand for coal and oil.

Buffett argues in favor of seeing climate change as a likely risk to the world, but against the need for more oversight, transparency or regulation of his companies. It’s a position he’s taken before -- Buffett argued against designating reinsurers, of which he owns the world’s fifth-largest, as too-big-to-fail institutions. Though he said he never spoke directly to regulators about the issue, he made his views public. Regulators, thus far, have agreed.

Why Buffett's Words Matter

Markets, governments and companies aren’t properly pricing the risk of climate change. For instance, are beachfront homes in low-lying areas as valuable as their owners believe? Experts reckon that only once markets and others attach a price to the threat of climate change will the rest of the world finally move to limit the potential consequences. If insurers -- which must grow their assets in order to make good on their guarantees -- measure the potential losses they could incur as a result of climate change, they can then price that risk. Then everyone else could follow.

Buffett's views against disclosure put him in sharp disagreement with Bank of England Governor Mark Carney, who has said that financial markets can help limit the effects of climate change, but only if companies -- such as insurers -- supply the kind of information that Buffett doesn't want to disclose.

In September remarks to the insurance industry, the chief overseer of the world’s third-largest insurance sector warned about the numerous economic and financial risks posed by climate change. Carney urged companies, particularly insurers, to start taking seriously their responsibility to measure their potential losses. Their own solvency could be at stake, Carney warned.

Insurance companies invest their money in places like the stock market. But “stranded" oil, gas and coal reserves, left in the ground due to the world’s commitment to halt rising temperatures, could render related financial assets worthless. Or the disruption of trade resulting from an extreme weather event could affect related investments.

Cynthia McHale, director of the insurance program for Ceres, a nonprofit group that pushes investors to pay attention to the financial risks of climate change, said in an interview earlier this month that neither insurers nor their government overseers have a good handle on the risks that climate change poses to insurers’ various financial assets.

McHale compared the situation to the one faced by big banks in 2008, when few sufficiently realized the magnitude of potential losses from the U.S. property bust.

Weathering Heights

Buffett's case against the resolution boils down to this: “Thinking only as a shareholder of a major insurer, climate change should not be on your list of worries.”

First, he said, his company can handle any possible losses thanks to rising premiums. Because insurance policies are typically written for one year and repriced annually, Buffett's company can hike premiums to better account for the heightened risk of climate change-driven losses.

Second, Buffett asserts that climate change has produced neither “more frequent nor more costly hurricanes nor other weather-related events covered by insurance.”

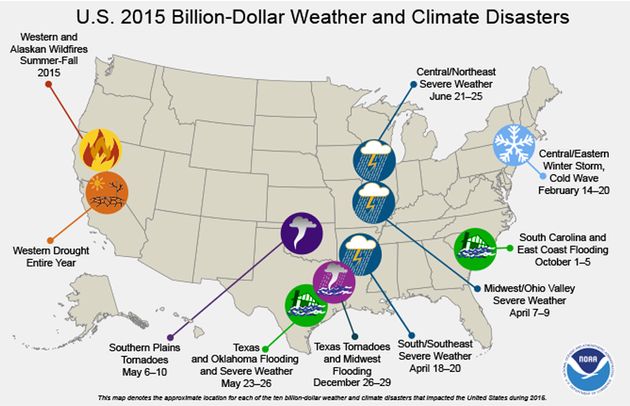

But eight of the 10 costliest hurricanes in U.S. history, in terms of insured losses, have occurred since 2000, according to the Insurance Information Institute. Nine of the 10 costliest floods in U.S. history, when measured by payouts from the federal government’s National Flood Insurance Program, also have occurred since 2000, according to the insurance group.

Munich Re, the world’s biggest reinsurer, estimated that extreme weather events led to $510 billion in insured losses from 1980 to 2011.

Carney said that according to Lloyd’s of London, the world’s oldest insurance market, the roughly 8-inch rise in sea level at the tip of Manhattan since the 1950s increased the insured losses from Hurricane Sandy by 30 percent in New York alone.

Insurance companies should care about climate change from a selfish perspective if they want to stay in business. Carney has warned that insurers that jack up premiums or exit markets after realizing the potential losses associated with climate change could unwittingly cause the value of their own assets to shrink.

He also warned about potential losses from claims on policies written by insurers. For example, insurance companies could be forced to make massive payouts if victims of climate change successfully hold accountable companies that contributed to it. He likened the situation to the one faced by U.S. insurers stung by tens of billions of dollars in losses from asbestos claims.

In fact, Carney said that as a result of recent weather trends, some now estimate that insurers are undervaluing their potential losses by as much as 50 percent.

Insurance companies caught unprepared for the effects of climate change could cause problems for government officials and put taxpayers at risk.

For example, governments may have to cover markets that insurers dump as a direct result of climate change, the Bank of England chief said, putting taxpayers on the hook.

What Could Change If Insurers Opened Up About This Risk

Disclosing climate change information would improve policymaking, Carney said. It could make climate policy more like monetary policy, where officials who set interest rates often tinker with their stance based on markets’ reactions.

The Financial Stability Board, a global group of the world’s financial regulators, wants financial companies to disclose their risks, too.

Some state insurance regulators in the U.S. are demanding insurers take the threat posed by climate change into account when investing their customers’ money and underwriting insurance policies. Washington state’s insurance regulator, Mike Kreidler, has criticized some insurers for failing to take climate change risks seriously, arguing their own solvency was at risk.

Buffett sounded more alarmed by the prospect of climate change in 2007, when scientific evidence of the impacts of climate change was less well-understood. In his annual letter that year, Buffett wondered aloud whether the deadly and expensive hurricanes of 2004 and 2005 marked the first warning of a new type of climate.

“It would be a huge mistake to bet that evolving atmospheric changes are benign in their implications for insurers,” Buffett wrote in his letter.

He warned that it was “naïve” to think of Hurricane Katrina -- the costliest hurricane in U.S. history -- “as anything close to a worst-case event.”

“These could rock the insurance industry,” Buffett added.

Original Article

Source: huffingtonpost.com/

Author: Alexander C. Kaufman, Ben Walsh, Shahien Nasiripour

No comments:

Post a Comment